Michael Vi/iStock via Getty Images

KKR Real Estate Finance (NYSE:KREF) last declared a quarterly cash dividend of $0.43 per share, in line with its prior payment and for a 16.6% forward dividend yield. Although this quarterly payout has been in place since the second quarter of KREF’s fiscal 2018, the yield has been pushed up to a record high on the back of a 47% decline in the commons over the last year. The mortgage REIT originates and acquires senior loans secured by commercial real estate with a tilt towards multifamily and industrial properties which formed 57% of its loan portfolio as of the end of its fiscal 2023 first quarter.

Commercial real estate, specifically office, is going through painful times as investors extrapolate the impact of entrenched remote working on rising occupancy. Bears, who form the 5.8% short interest are currently winning the battle for the inherent fate of the asset class as a still-rising Fed funds rate works to disrupt the capital market, raising the cost of funding for mortgage REITs and raising the specter of a recession. Is KREF a buy at its current level? Perhaps. Its shareholders would be right to highlight the mREIT’s record yield together with a 0.47x price to book, around 53% lower than its peer group median. Whilst the mREIT is externally managed, KKR is a premier private equity firm with $504 billion in assets under management and a 47-year operating history. KKR also owns 14% of KREF.

A Material Discount To Tangible Book Value

KREF’s discount to tangible book value (“TBV”) has widened to what could prove to be retrospectively unhealthy levels. TBV per share for its first quarter came in at $21.90, up sequentially from $20.56 and a 9.8% decrease from the year-ago quarter. The company’s common shares are currently changing hands for $10.38, a marked 52.6% difference from their intrinsic value.

This gap was essentially nonexistent in the period before inflation started running hot and the Fed was forced to respond with a series of consecutive rate hikes that have taken the Fed funds rate to its highest level in well over a decade. Hence, whilst interest rates are likely to remain elevated through 2023, there could be a case made for building a position in KREF on a reversion of interest rates to lower levels. This has placed distributable earnings and its ability to support the currently elevated dividend into view.

KKR Real Estate Finance Trust

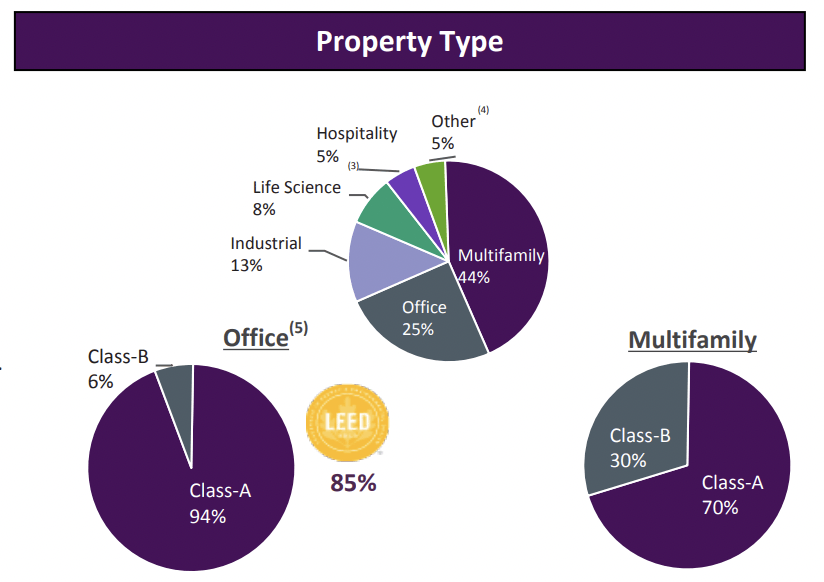

KREF’s fiscal 2023 first quarter brought in revenue of $51.16 million, an 8.4% increase from the year-ago quarter and a beat by $4.1 million on consensus estimates. This was powered by a loan portfolio that is 100% floating to remove interest rate risk. The portfolio is also fairly well diversified with office properties, of which 94% are Class-A, only accounting for a quarter of total loans.

First-quarter distributable earnings per share was $0.48, up around $0.01 from $0.47 in the year-ago comp and a beat by $0.02 on consensus estimates. This meant an 89.58% payout ratio against the current dividend. Whilst covered, it’s running tight and a recession could form a near-term headwind to portions of the loan portfolio being serviced. I think a dividend cut is unlikely, but a double-digit yield would likely still transpire post-cut.

The Series A Preferreds

KKR Real Estate Finance 6.50% Series A Cumulative Preferred Stock (NYSE:KREF.PA) offers a $1.625 annual coupon for a double digit 10.14% yield on cost. Whilst the roughly 645 basis point difference to the common’s dividend yield is not attractive, the Series A is also trading on a marked difference to their par value with around three years left to their April 16, 2026 redemption date. Critically, these form a safer source of income in the medium to long term against the specter of a recession and broader economic discombobulation from elevated interest rates.

QuantumOnline

They’re currently trading for $16.02, around an $8.98 difference, and a 36% discount to their redemption value. This gap to par began to widen markedly around the same time the commons started to diverge from their TBV to underscore just how much of a headwind to valuation expansion the mREIT will face as long as the macroeconomic environment continues to be defined by inflation and a hawkish Fed.

Critically, their yield to call currently stands at 22.9%, far ahead of the common’s yield to set the backdrop for the Series A owners over the next few years. Preferreds typically anchor around their par value with dislocations normally temporary when viewed through the lens of time. This is a long-term hold and I think performance should be healthy once current angst around commercial properties becomes more reasonable. The current fat yield covered has rendered the commons a possible buy once the rate hikes stop.

This post was originally published on this site be sure to check out more of their content.